What is blockchain technology? NIST Report goes beyond the hype of the most disruptive technology of the decade

Everyone is talking about Bitcoin and cryptocurrencies. But what a lot of people may not be know is the underlying technology behind cyrptocurrency. Given many potential applications of blockchain, it is surprising that blockchain is not getting the same level of attention as Bitcoin or other crytocurrencies. According to a report from a research analyst at the Royal Bank of Canada (RBC), crypto and blockchain technology could unlock $10 trillion market. A lot has been written about blockchain technology. In a simple term, blockchain is a special type of a distributed ledger database. A distributed ledger is simply a database that exists across several locations or among multiple participants. A distributed ledger system allows organization of any chain of records or transactions without the need of intermediaries.

But what exactly is blockchain? Today we want to answer this question by taking a closer look at the latest report from the National Institute of Standards and Technology (NIST). NIST is a non-regulatory agency of the United States Department of Commerce with a mission to promote U.S. innovation and industrial competitiveness by advancing measurement science, standards, and technology in ways that enhance economic security and improve our quality of life. From the smart electric power grid and electronic health records to atomic clocks, advanced nanomaterial, and computer chips, countless products and services rely in some way on technology, measurement, and standards provided by the NIST. Businesses and individuals use these various products and services every day. NIST is the arm of the U.S government that ensures that these products and services are reliable, safe, and of the best quality.

According to NIST, the reoughly 60-page report was developed at the request of several stakeholders, agencies and customers. These stakeholders asked NIST to create a straightforward description of blockchain so that newcomers to the marketplace could enter with the same knowledge about the technology,” the agency said in a statement on its website.

This report is noteworthy because NIST recommendations are likely to influence the adoption and regulation of blockchain technology not just in the U.S. government but also shape and guide blockchain adoptin in the private industry. The report provides a straightforward introduction to blockchain. It is intended to provide a high-level technical overview of blockchain technology. It discusses its application for electronic currency as well as broader uses. It also looks at different categories and approaches for different blockchain platforms.

According to NIST report, “A blockchain is essentially a decentralized ledger that maintains transaction records on many computers simultaneously. Once a group, or block, of records is entered into the ledger, the block’s information is connected mathematically to other blocks, forming a chain of records. Because of this mathematical relationship, the information in a particular block cannot be altered without changing all subsequent blocks in the chain and creating a discrepancy that other record-keepers in the network would immediately notice. In this way, blockchain technology produces a dependable ledger without requiring record-keepers to know or trust one another, which eliminates the dangers that come with data being kept in a central location by a single owner.”

“Blockchain is a powerful new paradigm for business,” Yaga said. “People should use it—if it’s appropriate.” The question is when it is appropriate. As with any new tool, there can be a temptation to employ it purely for its novelty value. The report outlines some possible use cases, including banking, supply chain management and keeping track of insurance transactions. The report, Yaga said, was created partly to help IT managers make informed decisions about whether blockchain is the right tool for a given task. “In the corporate world, there’s always a push to adopt new technologies,” Yaga said. “Blockchain is today’s shiny new toy, and there’s a big push to adopt it because of that.” “We want to help people to see past the hype,” he said, “as lofty a goal as that is.”

The report is organized into 10 sections.

- Section 1 provides the introduction to blockchain

- Section 2 defines the high-level components of a blockchain system architecture, including hashes, transactions, ledgers, blocks, and blockchains.

- Section 3 discusses how a blockchain is expanded through the addition of new blocks representing sets of transactions.

- Section 4 examines the need for consensus models to resolve conflicts among blockchain mining nodes.

- Section 5 introduces the concept of forking.

- Section 6 defines and discusses smart contracts.

- Section 7 looks at blockchain permission models, discusses their application considerations, and provides use case examples for each model.

- Section 8 provides several examples of blockchain platforms in use today to indicate the variations from one platform to another.

- Section 9 highlights some of the limitations of blockchain technology.

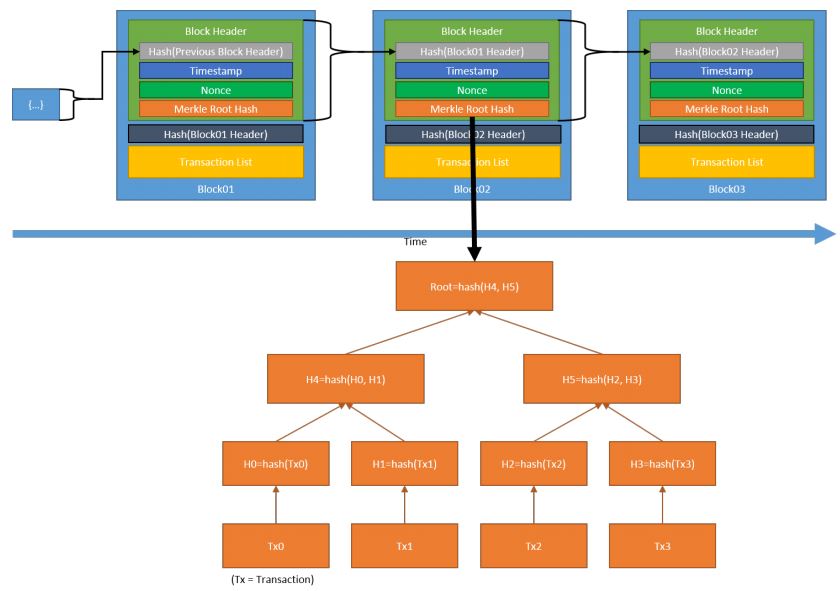

Example of a Blockchain with Merkle tree – Merkle tree is a data structure where the data is hashed and combined until there is a singular root hash that represents the entire structure.

The report might enlighten anyone who wants a picture of blockchain that is not skewed to any players’ interests, but Yaga said he and his co-authors hope it will give perspective to technical decision makers in particular.

“We don’t have any axe to grind or product to sell, though,” Yaga said. “A lot of articles you’ll read online feature a disclaimer indicating that the author owns a certain amount of cryptocurrency or stock in a company. I have no vested interest in the monetary value of these networks. But we don’t pass judgment on the technology; we just want to get past the rumors.”

“A company’s IT managers need to be able to say, we understand this, and then be able to argue whether or not the company needs to use it based on that clear understanding,” he said. “Some people are saying you should use it everywhere for everything. We wrote with the perspective that you shouldn’t use it if it’s not necessary.”

In the end, the report strives to help businesses make good decisions about when and if to use blockchain. The NIST report’s authors hope it will be useful to businesses that want to make clear-eyed decisions about whether blockchain would be an asset to their products. “We want to help people understand how blockchains work so that they can appropriately and usefully apply them to technology problems,” said Dylan Yaga, a NIST computer scientist who is one of the report’s authors. “It’s an introduction to the things you should understand and think about if you want to use blockchain.”

In conclusion, the report closes with recommendations, opportunities, potential use cases and applications of blockchain technologies. Blockchain has the power to disrupt many industries and the need for companies to proceed with caution. The report also concluded that blockchains are a significant new avenue for technological advancements, enabling secure 1276 transactions without the need for a central authority. The use of blockchains is still in its early stages, but it is built on widely understood and sound cryptographic principles. Moving forward, it is likely that blockchains will be another tool that can be used to solve newer sets of problems with blockchain digitizing assets other than just money.

Trending Now

Top Tech News Today, April 2, 2026