Crypto lending platform SALT pauses withdrawals and deposits; “Sorry the collapse of FTX impacted our business”

It’s just Tuesday and it’s looking like the repeat of last week. Last week, crypto lender BlockFi suspended withdrawals as fear of insolvency and liquidity crunch spreads across crypto markets. Then this week, BlockFi is preparing for bankruptcy, forming a new pattern with crypto-based companies.

As we finished reporting about BlockFi, there is a new trouble brewing at SALT, a crypto lending platform that provides blockchain-backed loans.

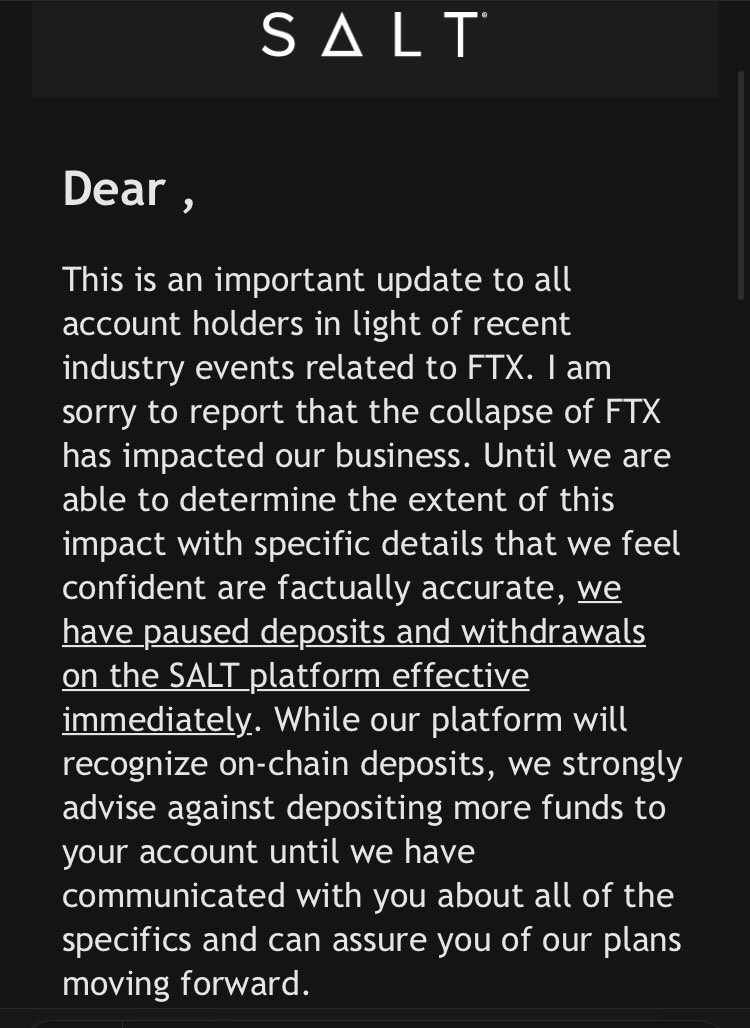

In a notice to its customers, SALT said it’s pausing all withdrawals and deposits, citing exposure to the now-bankrupt crypto exchange FTX. In a statement, SALT founder Shawn Owen apologized to the company’s customers saying “I’m sorry to report that the collapse of FTX impacted our business.”

A Twitter user Coffeezilla later tweeted that “Salt lending goes bust.”

Responding to the tweet, SALT CEO said the company did not publish the notice of going bust but pausing to deal with the fallout of FTX.

“We did not publish this as a notice of going bust. We are pausing to deal with the fall out of FTX and to confirm that non of our counter parties have any additional risks so that we can proceed with maximum caution with all efforts directed at not going bust. More info soon.”

We did not publish this as a notice of going bust. We are pausing to deal with the fall out of FTX and to confirm that non of our counter parties have any additional risks so that we can proceed with maximum caution with all efforts directed at not going bust. More info soon.

— Shawn Owen (@Shawn_OwenJ) November 15, 2022